Bond Total Return Calculator

Bond Investment Details

Additional Information

Total Return Results

Most people think they know how much their bonds are earning. They look at the coupon rate-say, 5%-and assume that’s their return. But if you only focus on the coupon, you’re missing half the story. Bonds don’t just pay interest. Their value moves with interest rates. And those interest payments? They don’t just sit in your account. They get reinvested. If you don’t account for all three pieces-yield, price change, and income-you’re flying blind.

What Bond Total Return Really Means

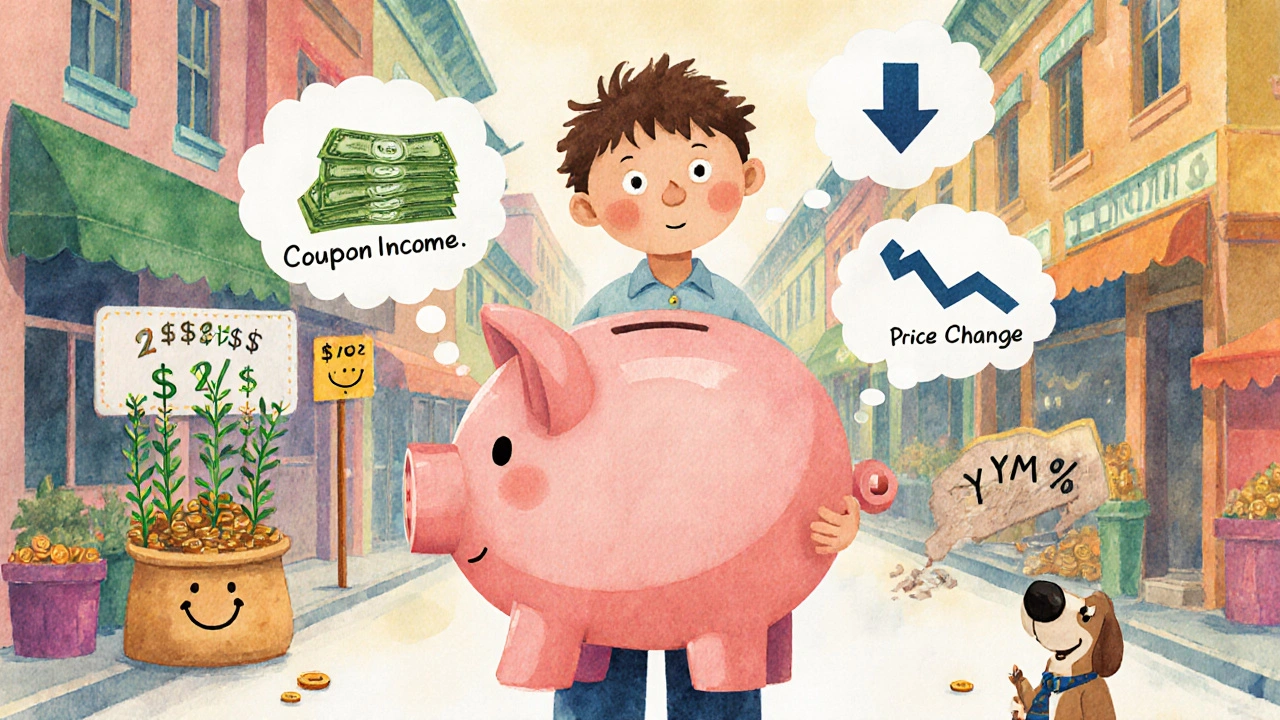

Total return is the real number. It’s what actually ends up in your pocket after holding a bond. It’s not a guess. It’s not a projection based on ideal conditions. It’s the sum of three things: the cash you collect from coupons, the gain or loss from selling the bond at a different price than you bought it, and the interest you earn by reinvesting those coupons. The bond market is huge-$128 trillion globally. And yet, most retail investors still use yield to maturity (YTM) as their main metric. That’s a problem. YTM assumes two things that almost never happen: you hold the bond until it matures, and you reinvest every coupon at the exact same rate as the YTM. In reality, interest rates change. Bonds get sold. Reinvestment rates drift up or down. That’s why total return matters more than ever.The Three Pieces of the Puzzle

Let’s break it down. Every bond’s total return comes from three sources:- Coupon income: The fixed payments you get every six months (or annually). For a $1,000 bond with a 5% coupon, that’s $50 per year.

- Price change: If interest rates rise after you buy, your bond’s market price drops. If rates fall, it goes up. This is capital gain or loss.

- Reinvestment income: The interest you earn on the coupon payments you reinvest. This is where most people get tripped up.

Why Yield to Maturity Lies to You

YTM sounds official. It’s printed on bond quotes. But it’s a theoretical number. It assumes you live in a perfect world where rates never move. If you buy a bond at a discount and hold it to maturity, YTM gives you a rough idea. But if you sell early-or if rates change-the YTM becomes meaningless. A 2022 Federal Reserve study showed that a 1% difference between your assumed reinvestment rate and the actual rate changes total return by 0.78% for a 10-year Treasury. That’s not small. For a $100,000 bond portfolio, that’s $780 a year-just from one percentage point error. On Reddit, a user named FixedIncomeNovice tracked his corporate bond portfolio over five years. He expected a 4.8% return based on YTM. His actual total return? 3.6%. Why? Because he reinvested coupons at 2.5% when the YTM assumed 4.5%. That gap cost him nearly 1.2% per year.How to Calculate Total Return (Without a PhD)

You don’t need MATLAB or a finance degree. Here’s the simple version:- Start with your purchase price.

- Add up all coupon payments you received during your holding period.

- Add the interest you earned by reinvesting those coupons.

- Add the sale price (or face value if held to maturity).

- Subtract your original purchase price.

- Divide by the purchase price.

- Annualize it over your holding period.

The Reinvestment Rate Trap

This is the biggest mistake investors make: using the bond’s YTM as the reinvestment rate. It’s tempting. It’s right there on the quote. But it’s wrong. In a rising rate environment, you’re likely reinvesting coupons at higher rates than the YTM. That boosts your total return. In a falling rate environment, you’re stuck reinvesting at lower rates. That crushes your return. The best way to estimate reinvestment rates? Use the current yield curve’s forward rates. These are market-implied expectations for future short-term rates. They’re not perfect, but they’re based on what thousands of traders are betting on-not your guess. A 2023 survey by FINRA found that investors who used forward rates for reinvestment assumptions had 1.4% higher portfolio returns over three years than those who used YTM.Tools That Actually Help

You can do this manually, but why? There are free tools that do it for you. - Vanguard’s Total Return Bond Calculator (launched September 2023) lets you plug in your bond holdings and pulls your actual purchase prices and coupon dates from your brokerage account. - Russell Cottrell’s Annualized Total Return Calculator is a simple web tool that asks for purchase price, coupon, holding period, and reinvestment rate. No login needed. - Morningstar’s fund screens now show total return as the default metric for bond funds-not YTM. Most brokerages now display total return in account summaries. If yours doesn’t, ask them. It’s 2025. This isn’t optional anymore.Why This Matters More Than Ever

Interest rates have been volatile since 2022. The 10-year Treasury swung between 3.5% and 4.9%. Bonds that looked safe at 4% suddenly lost value when rates jumped. Investors who only watched coupons got blindsided. The SEC now requires mutual funds to show total return alongside YTM in all marketing materials. That’s not a coincidence. It’s a response to years of investor confusion. Even more telling: J.P. Morgan predicts that by 2027, 92% of professional investors will use total return as their primary metric-replacing YTM entirely. If the pros are switching, you should be too.

Common Mistakes to Avoid

- Ignoring taxes: If you’re in a taxable account, your reinvestment rate should be after-tax. A 4% coupon might only net you 3.2% after federal and state taxes. - Using annual compounding: Most bonds pay semi-annual coupons. Use semi-annual compounding in your math. - Forgetting to update: Reinvestment rates change every month. Don’t set it and forget it. Re-run your calculation quarterly. - Assuming no price change: Even if you plan to hold to maturity, you might need to sell early. Always model price change scenarios.What Comes Next

The next big shift? Total return analysis will include ESG factors and inflation-linked bonds. That’s right-bonds tied to CPI are now 38% of the global market. Their returns aren’t just about coupons and price. They’re about inflation protection. That’s another layer to model. The SEC is also proposing a rule that would require all retail bond offerings to show a range of possible total returns-optimistic, base, and pessimistic-based on historical reinvestment patterns. That’s a huge step toward transparency. You don’t need to predict the future. You just need to understand what’s already in front of you. Total return isn’t magic. It’s math. And it’s the only way to know what your bond is really earning.Final Thought

A bond isn’t just a coupon. It’s a promise that includes price movement and reinvestment risk. If you treat it like a savings account, you’ll get surprised. If you treat it like an investment-with all its moving parts-you’ll make better decisions. Start calculating total return. Not next year. Not next quarter. Now.Is yield to maturity the same as total return?

No. Yield to maturity (YTM) is a theoretical estimate that assumes you hold the bond until it matures and reinvest all coupons at the same rate as the YTM. Total return is what you actually earn, including coupon payments, reinvestment income, and any price changes from selling the bond before maturity. YTM is a benchmark. Total return is reality.

How do I find the right reinvestment rate for my bond?

Don’t guess. Use the forward rates from the current yield curve. These are market-based expectations for future short-term interest rates. You can find them on the U.S. Treasury website or through free tools like Russell Cottrell’s calculator. Forward rates are more reliable than using the bond’s YTM or your personal forecast.

Do I need to calculate total return if I hold bonds to maturity?

Yes. Even if you hold to maturity, you still earn reinvestment income on your coupons. If interest rates fall after you buy, you’re reinvesting at lower rates, which lowers your total return. YTM assumes you reinvest at the same rate-but that’s rarely true. Total return gives you the real picture.

Can I use a free online calculator for bond total return?

Yes. Tools like Vanguard’s Total Return Bond Calculator (2023) and Russell Cottrell’s annualized return calculator are accurate and free. They handle compounding, reinvestment, and time periods automatically. Avoid basic coupon calculators-they don’t account for reinvestment income or price changes.

Why does my bond’s total return change even if I don’t sell it?

Because reinvestment rates change. Even if you hold the bond, each coupon you receive gets reinvested at the current market rate. If rates rise, your reinvestment income increases, boosting your total return. If rates fall, your reinvestment income drops, lowering your return. Total return is dynamic-it updates with the market.

I used to think YTM was the whole story until I actually tracked my bond portfolio over three years. Turned out my reinvestment rates were averaging 2.1% while my YTM said 4.3%. That 2.2% gap wiped out nearly $1,200 in expected gains. Now I use Russell Cottrell’s calculator every quarter-no more guessing. It’s embarrassing how long I ignored this.

Also, taxes matter. If you’re in a high-tax state, your after-tax reinvestment rate is way lower than you think. I started factoring in state taxes and my numbers finally made sense.

YTM is basically financial astrology. Like, ‘oh this bond says 5.2% so I’m rich!’ Nah. You’re not. You’re just holding a paper promise while the market laughs at you. I switched to total return tracking last year and my portfolio’s actual performance jumped 1.8%. No magic, just math.

And yes, Vanguard’s new calculator is a game-changer-pulls your purchase data auto-magically. My broker didn’t even show total return until I complained. 2025 and still acting like we’re in 2008. Wake up, people.

Let me be brutally clear: if you’re still using YTM as your primary metric, you’re not an investor-you’re a spectator. The Federal Reserve study alone should’ve been a sledgehammer to the skull. A 1% reinvestment error = $780/year on $100k. That’s a vacation. A car payment. A child’s tuition. And you’re ignoring it because it’s ‘too complicated’?

I’ve seen portfolios implode because people treated bonds like fixed-income savings accounts. Bonds move. Rates swing. Reinvestment isn’t a footnote-it’s the main event. The SEC is forcing transparency because retail investors have been systematically misled for decades. Stop being passive. Start calculating. Or get left behind.

It is truly fascinating how the human mind clings to simplicity even when complexity holds the truth. We are conditioned to seek single numbers-YTM, coupon rate, yield-that offer the illusion of control. But finance, like life, is not a single variable equation. It is a dynamic system where income, price, and reinvestment interact in nonlinear ways, shaped by global monetary policy, inflation expectations, and the silent drift of market sentiment.

I have observed, in my own modest portfolio, that even when holding to maturity, the reinvestment rate becomes a quiet thief-stealing returns slowly, almost imperceptibly, over time. The bond may promise 5%, but if the world offers only 2.5% for reinvestment, then the promise is hollow. The market does not care about our assumptions.

And yet, tools like forward rates from the yield curve, though imperfect, are our best compass. They are not guesses; they are collective wisdom distilled into numbers. I urge every investor, whether in Delhi or Denver, to move beyond the seduction of the coupon and embrace the full arithmetic of return. Not because it is easy, but because truth, however messy, is the only foundation upon which real wealth is built.

Perhaps one day, the SEC’s proposed range-based disclosures will become standard, not as regulation, but as ethical necessity. For now, let us calculate, let us question, and let us no longer be satisfied with the echo of a number that never was.