Carry Trade Risk Calculator

Calculate your potential gains and losses from a currency carry trade based on interest rate differentials, leverage, and market movements. This tool demonstrates why retail traders often lose money with carry trades.

Results

When you hear about making money just by holding a currency, it sounds too good to be true. And for most retail investors, it is. Currency carry trades promise easy returns: borrow cheap money in one country, invest it in another where interest rates are much higher, and collect the difference like free cash. But behind that simple math is a minefield of hidden risks that can wipe out your account in days-not months.

How Carry Trades Actually Work

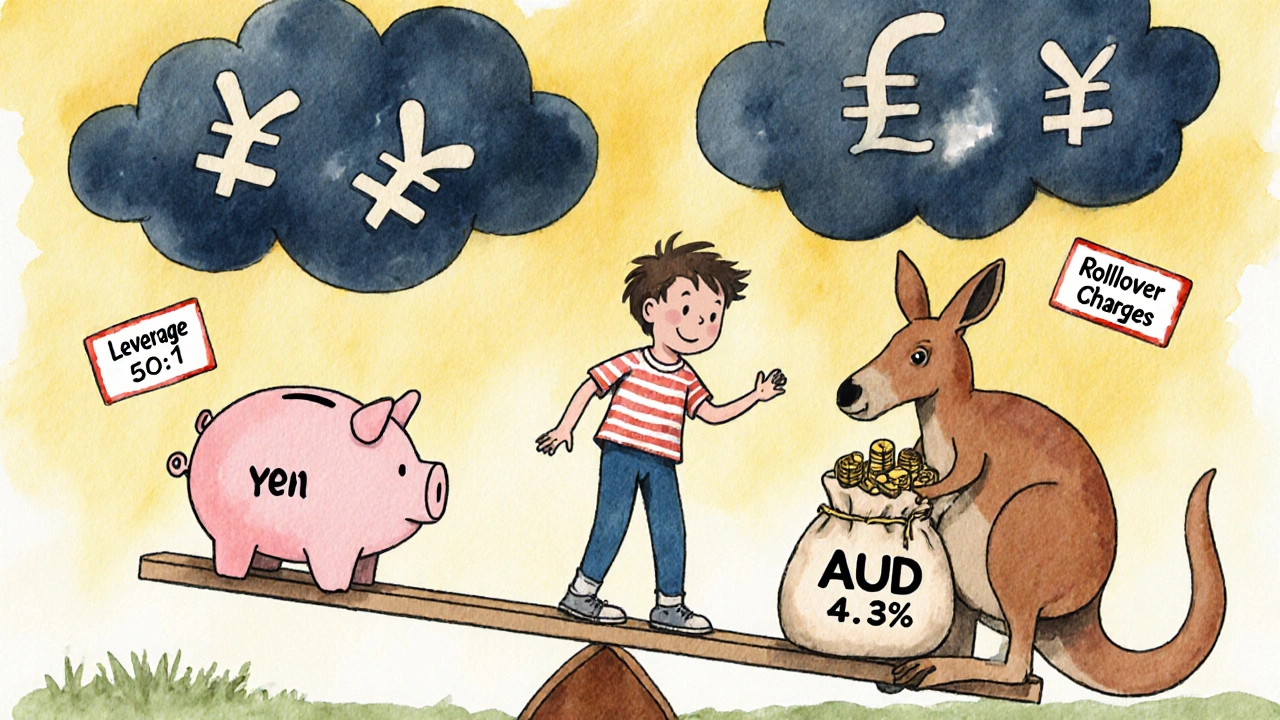

A carry trade isn’t about guessing if the euro will go up or down. It’s about exploiting interest rate gaps. You borrow Japanese yen, which has hovered near -0.10% for years, and use that cash to buy Australian dollars paying 4.35%. The difference-over 4% annually-is your profit, assuming nothing else changes. You don’t need the AUD to rise. You just need it to stay stable while you collect daily interest payments.

This strategy exploded in the 2000s, especially among Japanese retail traders. With domestic savings earning almost nothing, they turned to forex brokers offering 50:1 or even 100:1 leverage. That means a $1,000 deposit could control $100,000 in AUD/JPY positions. The math looked perfect: 4% annual return on $100,000 = $4,000. Even after paying broker fees, you’re still ahead.

But here’s the catch: currencies don’t move in isolation. When global fear spikes-like during the 2008 crash or the 2020 pandemic-investors dump risky assets and scramble into safe-haven currencies like the yen or Swiss franc. That’s when carry trades unravel.

The Silent Killer: Leverage

Most retail investors don’t realize that leverage multiplies losses just as fast as it multiplies gains. A 2% move against your position with 50:1 leverage doesn’t just cost you 2%. It costs you 100%. One bad day can erase your entire account.

In August 2007 and late 2008, Japanese retail traders lost 50-70% of their capital overnight as the yen surged 25% against major currencies. The same thing happened in 2022. Traders holding long positions in South African rand against the yen, with 50:1 leverage, saw 30-50% losses in weeks. One Trustpilot review from March 2024 described losing $8,500 in three days when the Turkish lira dropped 15% against the dollar. His position? Funded by shorting yen with 30:1 leverage.

The problem isn’t just the size of the trade. It’s the speed. When markets panic, liquidity vanishes. Bid-ask spreads for retail traders widen from 2 pips to over 100 pips. Your stop-loss order doesn’t execute at the price you set-it executes at whatever the market is dumping at. You get filled at a loss you never saw coming.

It’s Not Just About Interest Rates

Many beginners think carry trades are safe if they pick “stable” high-yield currencies. But stability is relative. The Mexican peso pays 10.5% interest, which looks great compared to Japan’s near-zero rate. But inflation in Mexico is still 4.7%. Central banks raise rates to fight inflation, not to reward investors. If inflation drops, the central bank cuts rates-and your carry trade income disappears.

And then there’s the Turkish lira. In June 2024, it offered a 50% interest rate. Sounds amazing, right? But that rate was a desperate attempt to stop the currency from collapsing. Inflation was over 64%. The lira lost 40% of its value against the dollar in just six months. Traders who held long lira positions didn’t get rich-they got liquidated.

High interest rates often signal economic weakness, not strength. The market knows this. That’s why high-yield currencies tend to fall sharply during global stress. Research from Georgia Tech shows high-yield currencies drop an average of 3.2% during market jumps, while low-yield currencies like the yen only drop 0.8%. That 2.4% gap wipes out months of interest income in one day.

The Unseen Cost: Rollover Charges

Here’s a detail most retail guides ignore: when you reverse a carry trade, you pay interest-not collect it. If you’re long AUD/JPY and the yen starts rising, you might try to flip your position short. But now you’re shorting the high-interest currency (AUD). That means you’re paying the Australian interest rate every night. With AUD at 4.35% and JPY at 0.1%, you’re paying 4.25% annually just to hold that short position.

Now imagine shorting the Turkish lira (50% interest) against the yen. You’re paying 50% per year in daily rollover charges. For a $1 million position, that’s $1,370 per day. No retail account survives that for long.

And it gets worse. If you’re holding positions through major economic announcements-like U.S. CPI or Bank of Japan policy meetings-your drawdowns are 37% higher than traders who close before the news. Most retail traders don’t even know when these events happen.

Why Institutions Win and Retail Investors Lose

Institutional traders don’t rely on retail forex platforms. They use direct market access, NDF markets, and real-time hedging tools. Their transaction costs are a fraction of what retail traders pay. During normal times, institutions trade AUD/USD with a 1-pip spread. Retail traders? 3-5 pips. During stress, institutions face 10-20 pips. Retail traders? 50-100 pips.

According to the Bank for International Settlements, institutional investors earn an average of 4.2% annually on carry trades. Retail traders? 2.1%. That’s not because institutions are smarter. It’s because they can move faster, pay less, and hedge better.

And they don’t gamble with 50:1 leverage. They use tight stop-losses, position sizing, and volatility filters. Retail traders? They see a 10% yield and go all-in.

What’s Happening Right Now (2025)

The yen carry trade is back-and it’s more dangerous than ever. Between January and July 2024, the yen rose 12% against the dollar. Why? Because the Bank of Japan signaled it might end negative rates. Bloomberg estimates a 65% chance of a rate hike to 0.25% by December 2024. That’s enough to trigger a massive unwind.

As of June 2024, retail traders held 185,000 net long contracts on AUD/JPY with average leverage of 33:1. When the pair dropped 15% in July, those positions lost an estimated $1.2 billion. And this was just the beginning.

The Federal Reserve may cut rates later in 2024, reducing the dollar’s appeal as a funding destination. Meanwhile, the European Central Bank and Bank of Japan are both moving toward normalization. The gap that once made carry trades profitable is closing.

The International Monetary Fund estimates a full unwind of global carry trades could trigger $300-500 billion in forced selling. Retail investors account for 15% of that exposure. That’s not a small number. It’s enough to cause panic.

What Should You Do?

If you’re thinking about a carry trade, ask yourself this: Do you understand what happens when the yen surges 15% in a month? Do you know how much you’d lose with 30:1 leverage? Have you tested your strategy through the 2008 crash and the 2022 volatility?

Most retail traders don’t. And that’s why 68% of those who trade carry strategies report net losses over a 12-month period-with average losses of 22.7% of their capital. That’s worse than the overall retail forex loss rate of 62%.

There’s no magic formula. No secret indicator. Just cold, hard math: high returns = high risk. And for retail traders, the risk isn’t just volatility. It’s leverage. It’s spreads. It’s rollover charges. It’s being last in line when the market turns.

If you still want to try it, start small. Use no more than 5:1 leverage. Avoid currencies with inflation above 10%. Never hold through major news events. And always, always assume the trade can go against you in 48 hours.

Because in carry trades, the interest you collect is just the candy. The real cost? The whole box.

Can you make money with currency carry trades as a retail investor?

Yes, but only under very specific conditions: low leverage, stable high-yield currencies, and strict risk controls. Most retail traders lose money because they over-leverage, ignore volatility spikes, and don’t understand rollover costs. The data shows 68% of retail carry trade traders have net losses over a year.

Why is the Japanese yen so popular for carry trades?

The yen has been one of the cheapest currencies to borrow for over a decade, with interest rates near -0.10% since 2016. This made it the go-to funding currency for investors seeking higher yields in AUD, NZD, or MXN. But as the Bank of Japan prepares to raise rates in late 2024, the yen’s appeal as a funding currency is fading, triggering unwinds that hurt retail traders.

What currencies are safest for carry trades right now?

There’s no truly safe carry trade, but some are less risky. The Mexican peso (10.5% interest, 4.7% inflation) and Brazilian real (9.25% interest, 4.5% inflation) are more stable than Turkey’s lira or South Africa’s rand. Avoid currencies with inflation above 10% or central banks that intervene heavily. Even then, never use leverage above 5:1.

How does leverage make carry trades dangerous?

Leverage turns small currency moves into massive losses. With 50:1 leverage, a 2% drop in your chosen currency wipes out your entire investment. During the 2008 crisis, yen appreciation hit 25% in six months. Retail traders with 50:1 leverage lost 100% of their capital instantly. Even 10:1 leverage can destroy an account during sudden volatility.

What happens when a carry trade unwinds?

When global fear rises, traders rush to sell high-yield currencies and buy safe-haven currencies like the yen or Swiss franc. This forces a sharp drop in currencies like AUD, ZAR, or TRY. Traders holding long positions get liquidated. Those who flipped to short positions face massive rollover charges. The result? A cascade of forced selling that can trigger billions in losses across markets.

Are carry trades still worth it in 2025?

For most retail investors, no. The interest rate gaps are shrinking as central banks normalize policy. Volatility is up 40% year-over-year. Leverage is still dangerously high among retail traders. The potential rewards don’t justify the risk of losing everything in a single market event. If you’re not a professional with institutional tools, avoid carry trades entirely.

It's fascinating how the allure of passive income blinds so many to the structural fragility of these trades. The interest rate differential isn't a reward-it's a compensation for risk, and retail investors are often the ones left holding the bag when the global risk appetite evaporates. I've watched this cycle repeat since 2008: the yen strengthens, the carry trade implodes, and suddenly everyone's asking why they didn't see it coming. But the truth is, they did see it-they just hoped the math would work out anyway. There's a deeper human tendency here: we're wired to chase yield, even when the system is rigged against us. The real tragedy isn't the losses-it's that the same people who lose money are the ones who get marketed to the hardest, told that this time is different, that they're smart enough to time it, that leverage is just a tool. But tools don't care if you're ready. And markets don't care if you're sincere.

Bro, the whole carry trade thing is just arbitrage with extra steps and way more drama. You're basically borrowing cheap debt and betting on FX stability while collecting yield like a coupon clipper. But here’s the kicker-retail traders don’t even understand what ‘basis risk’ means. They see 50% yields on TRY and think they’re hitting the jackpot. Meanwhile, the central bank’s printing money like it’s Monopoly and the currency’s value is held together by duct tape and hope. And don’t get me started on leverage-50:1 is just gambling with someone else’s margin call. Institutions don’t play this game because they know it’s a volatility dumpster fire. Retail? They’re the trash in the dumpster.

Oh wow, a 68% loss rate? Groundbreaking. I’m shocked-shocked!-that people who think ‘carry trade’ is a new Netflix series are losing money. Let me guess: they read a Medium post titled ‘How I Turned $500 Into $50,000 With Japanese Yen & Pure Vibes’ and thought, ‘This is my sign.’ Look, if you’re using 30:1 leverage on a currency with 64% inflation, you’re not investing-you’re performing a financial magic trick where the rabbit is your entire life savings. And you’re the magician. The only thing more pathetic than your strategy is your broker’s ‘educational content’ that makes it look like a side hustle. You’re not a trader. You’re a demographic. A metric. A line item in a hedge fund’s profit report. Congratulations-you’re the sucker in the system.

Thanks for this. Really eye-opening. I used to think high yields = safe bets. Now I see it’s the opposite. I’ll stick to savings accounts. :)