Broker Fee Calculator

Your Potential Savings

Choosing between a discount broker and a full-service broker isn’t about which one is better-it’s about which one matches your life, your money, and how much you want to do yourself.

Back in the 1970s, if you wanted to buy stocks, you called a broker. They talked you through it, picked your investments, and charged you a chunk of your portfolio just to execute the trade. Today, you can open an account in 10 minutes, trade for free, and watch your portfolio move on your phone. But that doesn’t mean the old way disappeared. In fact, both models are thriving-just for very different people.

What You Get (and Don’t Get) With Each

Full-service brokers like Morgan Stanley, Merrill Lynch, and Edward Jones act like financial doctors. They run full checkups on your money. That means retirement planning, tax strategies, estate plans, insurance reviews, and even helping you talk to your kids about inheritance. They assign you a dedicated advisor who knows your name, your goals, and your fears. You get face-to-face meetings, usually four to six times a year, and they adjust your portfolio based on your life changes-like a new job, a divorce, or aging parents.

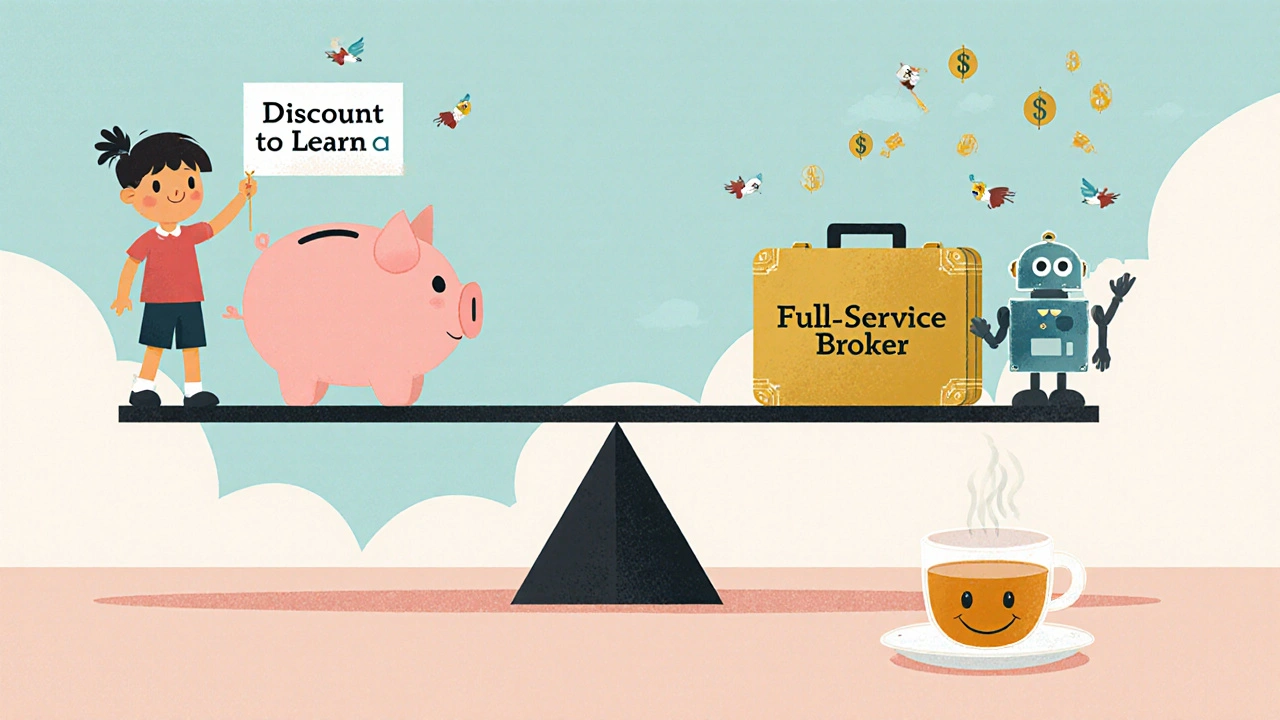

Discount brokers like Charles Schwab, Fidelity, and Robinhood? They’re more like a self-checkout lane at the grocery store. You pick what to buy, you scan it, and you pay. No one asks if you really need those chips. They give you tools: real-time charts, stock screeners, research reports, and mobile apps. But if you don’t know how to use them? You’re on your own. There’s no advisor sitting beside you saying, “Wait-why are you buying leveraged ETFs?”

Costs: The Hidden Killer

Full-service brokers charge you in two ways: commissions and asset fees. Most charge 1% to 2% of your total investments every year. If you have $100,000, that’s $1,000 to $2,000 annually-just to keep the door open. Add transaction fees on top, and you’re paying even more. Over 30 years, that 1% fee on a $100,000 portfolio growing at 7% a year costs you over $130,000 in lost returns. That’s not a small number-it’s the equivalent of losing a second home.

Discount brokers? Most charge $0 to trade stocks and ETFs. No commissions. No hidden fees. Account maintenance? Usually nothing. A few still charge $15-$50 a year, but even that’s rare now. You might pay $5-$10 for a mutual fund trade or a wire transfer, but those are exceptions. The real cost? Your time. If you don’t know how to research a company, track taxes, or rebalance your portfolio, you’re paying with stress-and maybe with losses.

Who Uses What-and Why

Here’s the hard truth: full-service brokers serve people with $1 million or more in investable assets. That’s 68% of their client base. These are people who need complex planning-trusts, business succession, multi-state taxes, charitable giving. They’re not trying to beat the market. They’re trying not to mess up what they’ve built.

Discount brokers? They’re for everyone else. 89% of retail investors with under $100,000 use them. That’s mostly people under 45. Millennials and Gen Z? 89% of them only use discount brokers. They grew up with apps. They trust algorithms. They don’t want to pay someone to tell them what they can Google.

But here’s what most people miss: discount brokers aren’t just cheaper-they’re designed for active traders. If you check your portfolio daily, trade weekly, and follow market news, you’ll love the speed and tools. If you just want to set up a 401(k) and forget it? You’ll feel lost.

The Human Factor: When You Need a Real Person

Markets crash. Your job disappears. Your parent gets sick. In those moments, you don’t want a chatbot. You want someone who knows your name and can say, “I’ve seen this before. Here’s what we do.”

Full-service brokers have advisors on call. J.D. Power found that clients get through to their advisor within 15 minutes during business hours. That’s huge when the market is dropping 5% and your stomach is in your throat.

Discount brokers? Support is email or chat. Response time? 2 to 24 hours. Phone support? Usually only if you have $25,000 or more. And even then, you’re talking to a call center rep-not your advisor.

There’s a reason Reddit’s r/investing has 47,000 members, but r/WealthManagement has under 3,000. Discount broker users build their own communities because they have to. They share tips, warn each other about bad trades, and help each other learn. Full-service clients? They rarely need to. Their advisor handles it.

What’s Missing: The Dark Side of Both

Discount brokers make money in ways you might not realize. About two-thirds of them earn revenue through “payment for order flow.” That means they sell your trade to high-frequency trading firms. It’s legal. But it creates a conflict: the broker wants you to trade more-even if it’s not good for you. You might not notice it, but your trades could be getting filled at slightly worse prices.

Full-service brokers? Their advisors are often paid on commission. That means they might push products that pay them more-not what’s best for you. In 2023, the SEC fined a major firm $12 million for pushing risky, concentrated stocks on elderly clients. The advisor got bonuses. The client lost money.

Both models have traps. The difference? One hides it in fine print. The other hides it in silence.

Who Should Choose Which?

If you’re under 35, have less than $50,000, and enjoy learning how the market works-you’re a discount broker user. You’ll save thousands over time. Use free tools from Fidelity or Schwab. Read their educational content. Start small. Make mistakes. Learn.

If you’re over 50, have $500,000 or more, have a complicated tax situation, or just don’t want to think about money anymore-you need a full-service broker. Don’t go cheap. Find a fiduciary advisor (legally required to act in your best interest). Ask how they’re paid. If they get commissions from selling products, walk away.

What if you’re in the middle? Maybe you have $200,000 and you’re not sure? Try a hybrid. Raymond James and some others now offer “wrap accounts” at 0.75% AUM. You get a little advice, a little automation, and lower fees. It’s not perfect-but it’s a bridge.

The Future: What’s Changing Fast

By 2027, McKinsey predicts 25% of investors will use hybrid models. That’s because robo-advisors like Betterment and Wealthfront are getting smarter. They now offer basic tax-loss harvesting, rebalancing, and even human advisor access for $2,500 a year. That’s cheaper than most full-service brokers.

Full-service firms aren’t sleeping. Morgan Stanley launched an AI tool in early 2024 that gives advisors real-time suggestions during client meetings. It cuts prep time by 37%. That means better advice-not less human interaction.

Discount brokers are adding research tools. Charles Schwab and Interactive Brokers now offer basic market analysis, earnings summaries, and even AI-driven “what-if” scenarios. You’re still on your own-but you’re not completely alone.

The SEC is pushing for new rules in 2025 that will force brokers to show you exactly how much you’re paying in fees-side by side. That’s going to shake things up. You’ll finally be able to compare apples to apples.

Final Thought: It’s Not About the Broker. It’s About You.

You don’t need a full-service broker because you’re rich. You need one because your life is complicated. You don’t need a discount broker because you’re broke. You need one because you want control.

Most people think this is a choice between expensive and cheap. It’s not. It’s a choice between outsourcing and owning. One gives you peace of mind. The other gives you power. Neither is right for everyone. But one is right for you-if you know what you’re asking for.

It's fascinating how the evolution of financial services mirrors our broader societal shift from hierarchy to autonomy-yet we rarely pause to ask whether autonomy truly liberates, or merely burdens us with the weight of choice. The discount broker model, for all its efficiency, assumes a level of financial literacy that many simply don’t have, not because they’re lazy, but because education was never designed to prepare them for this. Meanwhile, the full-service model, though costly, offers something irreplaceable: the quiet reassurance that someone else is holding the compass while you navigate the storm. Perhaps the real divide isn’t between brokers, but between those who see finance as a skill to master, and those who see it as a life to protect.

Let’s be real-payment for order flow is the financial industry’s version of selling your attention to advertisers. It’s not fraud, it’s just capitalism with a smiley face. And don’t get me started on how full-service advisors are basically glorified sales reps with fiduciary labels glued on like a sticker. If your advisor pushes annuities or load funds, they’re not your friend-they’re a commission-driven middleman with a handshake and a PowerPoint. The only way to win is to go DIY, educate yourself on index funds, and ignore the noise. The market doesn’t care how much you pay your advisor-it only cares if you’re diversified and patient.

Oh wow, a 10,000-word essay on how to not get scammed by people who get paid to not get scammed. Pathetic. The real issue isn’t discount vs. full-service-it’s that 98% of retail investors are emotionally unstable gamblers who think ‘buy the dip’ is a strategy. You don’t need an advisor to tell you not to buy leveraged ETFs-you need to stop being an idiot. And yes, I’m talking to you, the guy who bought Tesla at $1200 because a TikTok influencer said it’s ‘the future.’ The only thing worse than paying 1% to a clueless advisor is paying $0 to a clueless you. Congrats, you saved $2,000 a year and lost $200,000 in opportunity cost. That’s the real ROI.

Thank you for this. 🙏 I'm 32, have $45k, use Fidelity, and check my portfolio once a month. I don't know much, but I'm learning. It's scary, but I feel like I'm in control. Not perfect, but better than feeling lost.

There’s a quiet dignity in knowing your limits. I used to think hiring an advisor was a sign of weakness-until my dad lost half his retirement in 2008 because he trusted a friend who ‘knew the market.’ Now I see that financial peace isn’t about maximizing returns-it’s about minimizing regret. The hybrid model is the future for good reason: it gives you structure without dependency, tools without overwhelm. You don’t have to be a guru to be smart with money. You just have to be honest with yourself about what you’re willing to carry-and what you’re willing to let someone else hold for you.